The fiduciary duty

When looking for a financial advisor, make sure you pick one that owes you fiduciary duties.

Why? A fiduciary is required to act in your best interest. Financial advisors without fiduciary duties—including brokers, financial planners, and insurance agents—don’t have a fiduciary duty to act in your best interest when recommending investments or strategies to you.

Rather, many of them need only make a “suitable” recommendation to you: one that meets your investing objectives, even if much better, and less costly, alternatives exist. (Though this may be changing for brokers under “Regulation Best Interest”–more on that later).

This leaves the door open for a financial advisor to select an investment for you that earns them a high commission. How big of a problem are high-commission investments? According to a study by The White House Council of Economic Advisors, a big problem: financial advisors’ biases cost Americans $17 billion per year in losses.

The fiduciary rule set a high standard for brokers and insurance agents who work on commission.

In 2016, the Department of Labor issued a rule requiring certain financial professionals who give advice on retirement accounts to adhere to a fiduciary standard. In short, the rule said that if you’re working with someone who gives you advice about your 401(k), 403(b), IRA or other retirement account—and they’re getting paid commissions (or fees) for doing so—then they must now adhere to what’s known as the “fiduciary” standard when giving their recommendations: they must work in your best interest rather than simply trying to earn more from their own products/services by pushing something else on you instead.

This included brokers who sell mutual funds and annuities as well as insurance agents who sell life insurance or annuities through the workplace. Both brokers and insurance agents typically get paid commissions on the financial products they sell.

Under the rule, brokers and agents who still wanted to recommend those high-commission products would need to tell their clients that the investment would land the advisor a big commission. The advisors would also have to disclose to their clients exactly how much they were being compensated.

What does that all mean in practice? The rule would have made it impossible for advisors to recommend those high commission products in many cases. And the financial industry knew it, and feared it.

The fiduciary rule goes down in defeat.

After lawsuits and opposition by the brokerage industry, the rule was defeated. The brokerage industry complained that they would lose too much money if conflicts of interest, high commissions, and high-fee products were eliminated: over $5 billion ever year by some estimates.

Advisors can still be fiduciaries based on their relationship with you.

But even though the fiduciary rule was defeated, a financial advisor can still be a fiduciary. It depends on the relationship between the advisor and the client.

For example, the Illinois Supreme Court has explained that a “fiduciary relationship may arise as a matter of fact where one party reposes trust and confidence in another, who thereby gains a resulting influence and superiority over the subservient party.” Van Dyke v. White, 2019 IL 121452, ¶¶ 75-76 (The court found that because the financial advisor’s clients “had put their trust in him and relied on him for his investment advice,” the advisor “owed a fiduciary duty” to them “to act in the best interests of his clients.”).

And don’t forget that some financial professionals always owe you fiduciary duties. For example, Certified Financial Planners owe fiduciary duties to their clients and must put their clients’ interests first anyway.

Regulation B.I.–a proxy fiduciary rule?

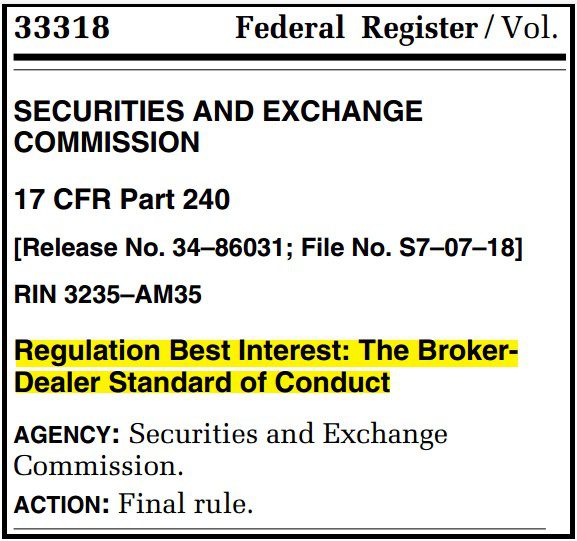

Although the fiduciary rule may have gone down, in June 2020, the Securities and Exchange Commission published a similar rule that applies to all brokers, called “Regulation BI,” which stands for “Best Interest.”

Regulation BI is intended to be a change from the suitability standard. Under Regulation BI, brokers are required to put their client’s best interest first when recommending a security or investment strategy. This sure sounds similar to what a fiduciary must do. But because Regulation BI is so new, it remains to be seen whether it will act force brokers to act more as fiduciaries in practice.

A brand new fiduciary rule in 2023?

The original fiduciary rule that was proposed in 2017 died after the Fifth Circuit Court of Appeals vacated it in 2018. But that is not the end of the story just yet. The White House says that will propose another fiduciary rule in 2023–one that it hopes won’t be overturned by a court.

So a new rule attempting to make all advisors adhere to the fiduciary standard may be on the horizon.

Contact us for more information

Whether or not your financial advisor is a fiduciary, if they mismanaged your investment account, they may be liable to you. Contact Wilkowski Law and receive a free assessment of your potential claim. Let us know how we can help.